We're back (finally!) with the final installment of our insights reports on the 2025 cannabis industry. We apologize for the delay, we had to shuffle some things around in the publication schedule. If you haven't yet checked out the Cultivation or Commercial reports, we recommend reading them as well for full context on the state of the industry. All data in this report is sourced from the California Unified License Search, a regularly updated public record of all State licensed operators past and present. Without further ado, let's dig into manufacturing!

California Cannabis Manufacturing Background

California requires licensees to hold a manufacturing license for most processing, preparation, and concentration of cannabis. There is a limited carve out for "Non-manufactured" cannabis goods that allows farms to make and packaged products that don't really require any alteration of the plant material- things like flower, shake, non-infused prerolls, and keif. Everything else requires a manufacturing license, either a standalone one or as an activity for a Microbusiness. There are five different license types for Manufacturing:

Type 6 (Non-Volatile): For making concentrates and extracts with non-volatile extraction processes, and for infusing.

Butters/Oils

Ethanol

CO2 extraction

Mechanical methods (Rosin press, dry ice, Ice water wash)

Type 7 (Volatile): For making concentrates and extracts with volatile extraction processes.

Butane, Heptane, and other volatile flammable solvents

Type N (Infusion): Allows infusion and mixing of cannabis materials or concentrates.

Edibles/Gummies/Drinks

Topicals/Creams/Cosmetics

Infused plant material prerolls

Type P (Packaging): Only allows the packaging of cannabis products, no manufacturing or modification of the cannabis material itself.

Type S (Shared): A hybrid license that allows multiple licensees to use a single space for certain activities. An existing manufacturer can convert some of their licensed space to be shared. An example would be an edibles kitchen or ice water hash/rosin lab that multiple different licensed growers run their material through.

Oil/butter extraction

Mechanical extraction

Infusion

Packaging

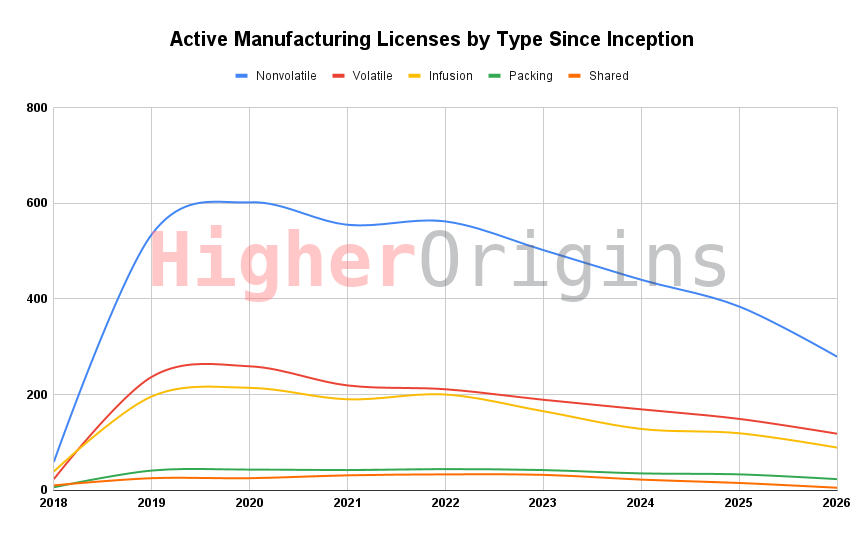

Statewide Manufacturing Trends

Now that we understand the licenses here, let's dig into the licensing numbers since legalization.

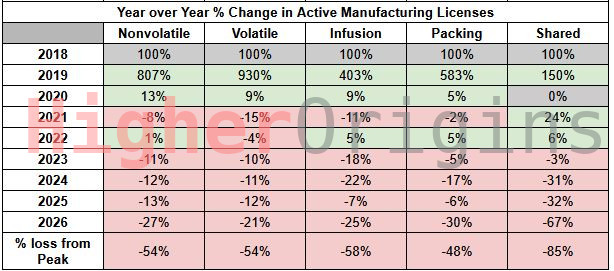

The manufacturing sector is the smallest and most stable category in the California industry. Across the top three most common license types, a common trend is clear. Licensing peaked early, in 2019 and 2020, and since then has declined across the board steadily, with the exception of a slight bump in 2022, possibly caused by a pullback and then reinvestment cycle caused by the pandemic. Nonvolatile is by far the most common category, likely because it allows for the creation of a wide variety of products without having to deal with the extra lab infrastructure involved with more advanced solvents. Infusion and volatile facilities are roughly equal, with slightly more volatile extractors. Packaging licenses have remained relatively constant over time, while the already rare shared use licenses have basically disappeared after peaking in 2022/2023.

When we look at the annual percent changes in licensing, we see that proportionally, shared use licenses have failed at the highest rate, especially recently. While this makes up a small sliver of the market, it may indicate a lack of investment cash available to smaller operators, which tracks with overall cannabis economy trends. Often, shared facilities are operated by collectives or associations of smaller operators who can't individually afford the overhead for a facility, or only use it seasonally. When free cash dries up, it may be more economical for shared operators to cut their losses and pay someone more established to process their weed. At this point, shared licensing seems practically extinct, with only 5 left statewide.

Of the more popular licenses, infusion licenses have lost the most proportionally, which makes sense. Non-volatile licensing can extract AND infuse under one license, while infusion facilities can only infuse and must source their cannabis material from an extractor. This means that infusers can make less and have to buy more raw materials, rather than being able to capitalize on their internal production. Being only a one-trick license is a liability in a competitive industry with thin margins.

Volatile manufacturers operate with high overhead due to the large amount of safeguards and special equipment they have to use for the more dangerous chemicals they work with. This overhead, combined with some consumer's distrust of the chemicals they use, may explain their drop over time, in addition to the overall negative economic headwinds and competition.

As the most popular license, non-volatile facilities are tied with volatile for proportional losses, but still account for the bulk of the industry, with 279 in operation in January 2026. While they are more flexible than infusion licenses and have less overhead than volatile extraction, these licenses are clearly prone to economic conditions and competition. As vapes and extracts become the preferred method of consumption, bigger players will race to consolidate their control over the manufacturing sector, upgrading their facilities to reach economies of scale over their smaller competition. There's no limit on how much product a manufacturer can process, and with vertical megafarm-to-distillation arrangements like LEEF's expansion, scale will dominate in most cases.

Packaging licenses have suffered the least proportionally, and remained the most stable category overall, largely supported by operations in LA. These licenses are in a pretty established niche and benefit by being downstream of every kind of manufacturing- regardless of what kind of product is made where, a packaging facility can still make money packing it up. Furthermore, labor for packaging is usually less specialized and requires less overhead to operate. On the flipside, other manufacturers, distributors, and farms can package products as well, so packaging licenses face a lot of structural competition.

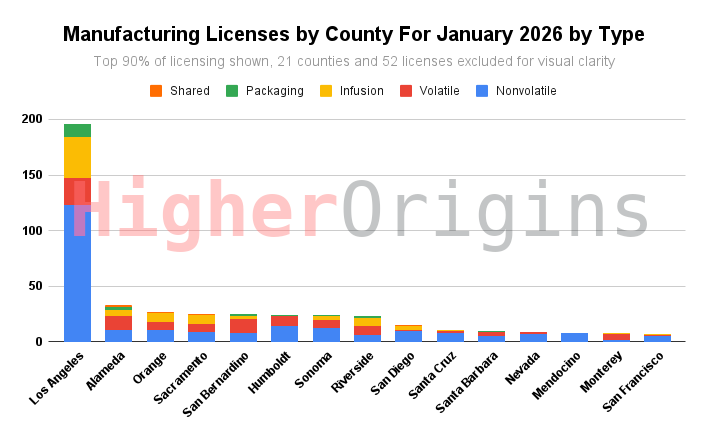

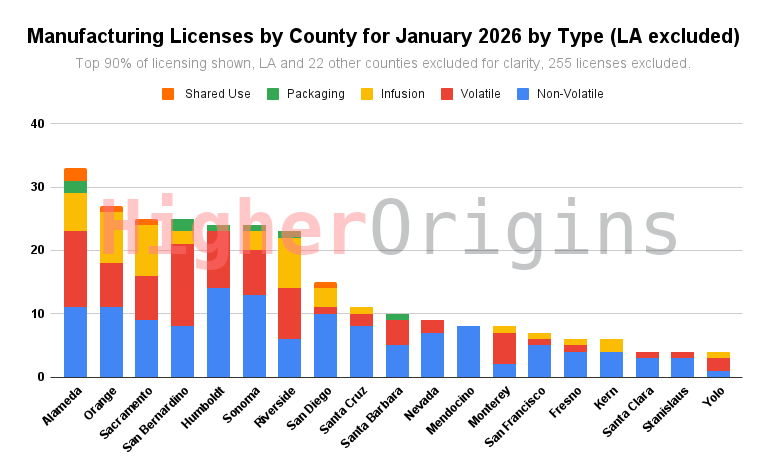

When we break down the distribution of current active licenses across the state, we see an obvious outlier: Los Angeles County has a massive presence in the manufacturing sector, and highly skews the numbers. In comparison with most other counties, the ratio of non-volatile extraction to other license types is a bit larger, possibly due to the difficulties of permitting and building out a volatile solvent lab in a mostly urban area with high permitting and real estate costs.

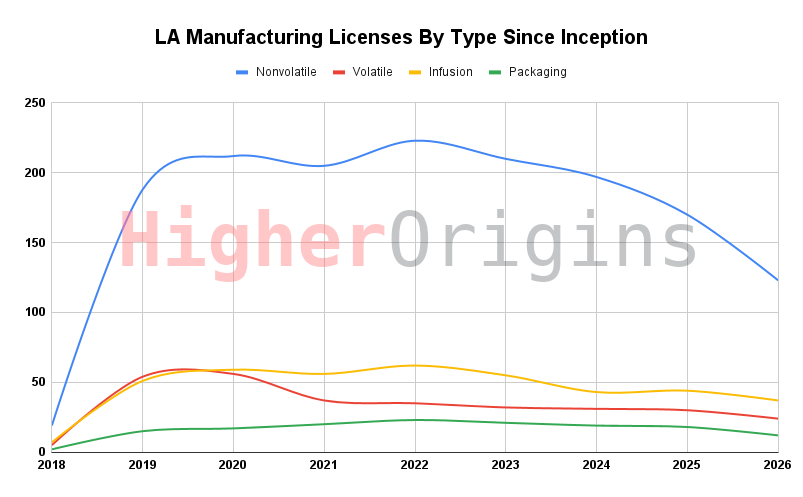

LA is such a big part of the manufacturing industry statewide that it may be helpful to look at the trend over time for just that county. Compared to the state, LA has proportionately way more non-volatile extraction, a more sudden downturn in volatile licensing around the pandemic that never recovered, and absolutely no shared spaces, even in the past. In the next charts, we will look at the rest of the counties in the state without LA included. When you look at these charts, keep in mind that LA is actually a lot more stable than the rest of the state, so regional license instability is balanced out in the state trendlines by LA.

County Trends in Manufacturing

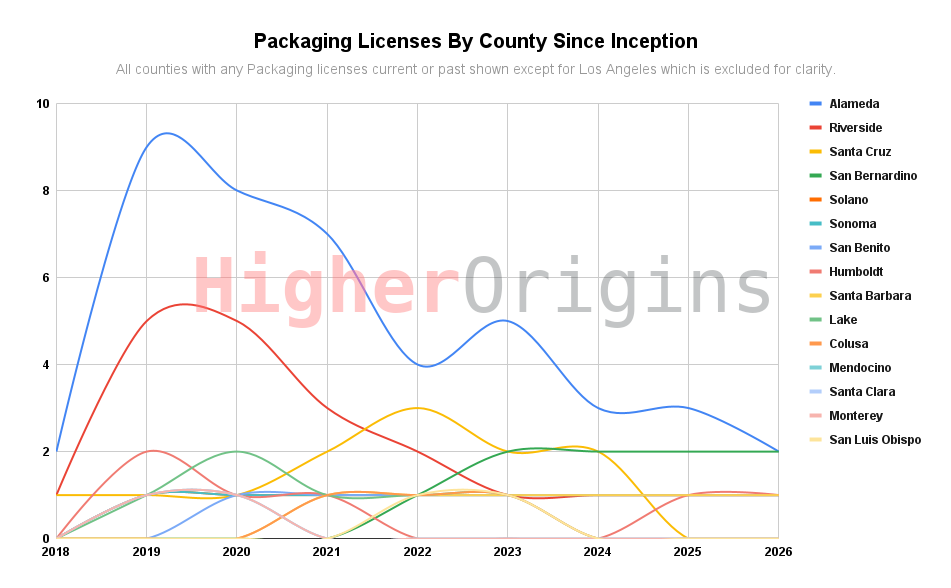

With our outlier removed, it's much easier to see what the rest of the state looks like in terms of licensing. Alameda county in the East Bay area leads the pack, with a balanced ratio of non-volatile to volatile operations. Notably, Alameda is the only county with more than one Shared license, speaking to the community collaborative nature of how the cannabis industry started in the county. Orange, Sacramento, San Bernardino, Humboldt, Sonoma, and Riverside counties all form a fairly equal group, with only Humboldt standing out significantly for their higher ratio of non-volatile licenses and no infusion operations. Clearly, it makes more sense for the flower and concentrates focused export economy of the redwood region to export raw materials to edibles kitchens in the Bay and Southern California. This trend towards non-volatile is mirrored in our own Mendocino county, which comes after Nevada county in the single-digit manufacturing licenses.

License Categories Regionally Since Inception

We can further explore trends in licensing across the state by tracking the top counties in each manufacturing category over time.

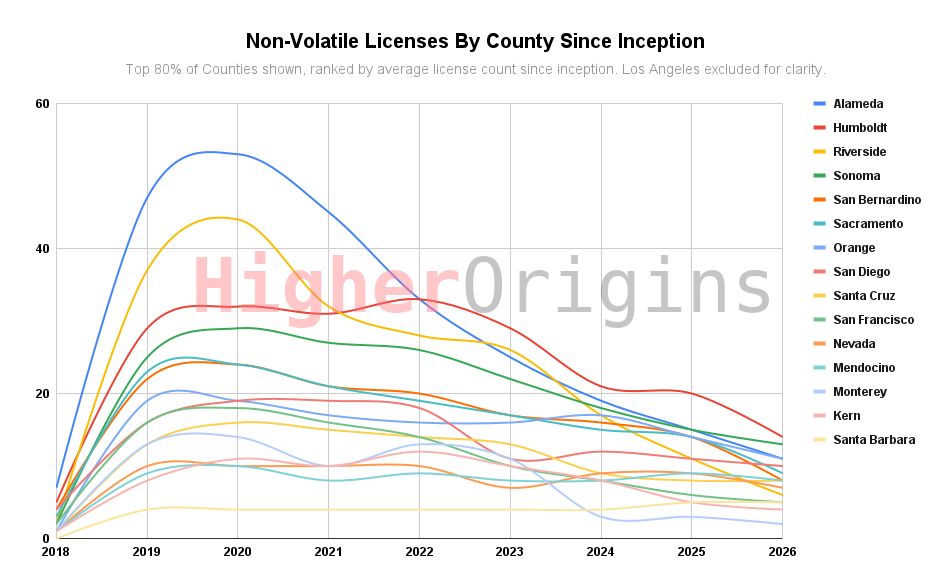

As the biggest category, non-volatile has the messiest chart. The trends seems universally downwards across the board, with only a few off-trend bumps in Humboldt, Riverside, Orange, Monterey, San Bernardino, and San Diego really standing out. One or two counties are relatively flat going into 2026, suggesting they may have found market equilibrium, but there's little to suggest that a generalized growth trend will materialize. Santa Barbara bucks the trend, maintaining a balanced market for years before experiencing a slight boost. This is likely due to the large farms in the area that feed a small but secure population of manufacturers- steady local supply from well-capitalized farmers is a good recipe for stability.

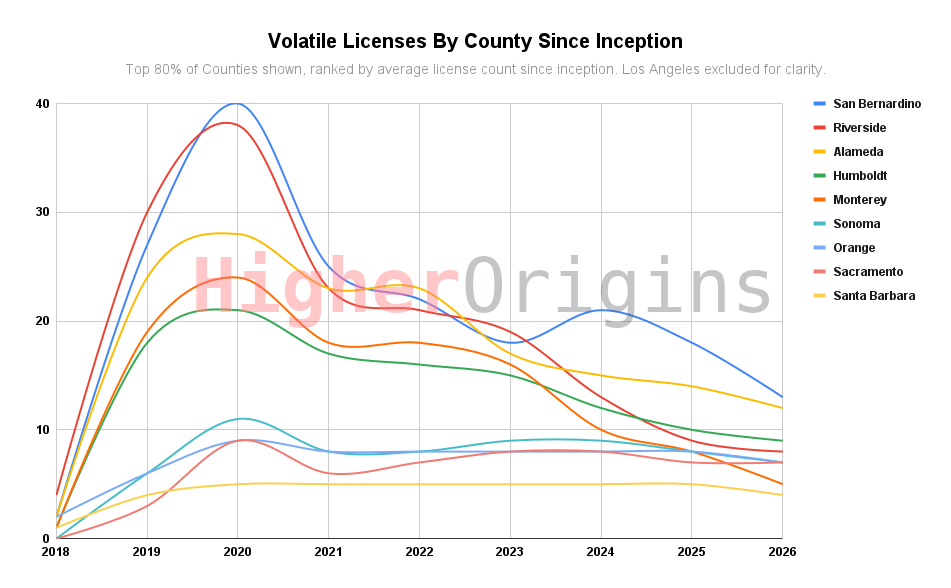

Volatile licensing is on a downtrend, but the loss has been less consistent, with some regions seeing periods of stability since the parabolic losses of 2020. In fact, some of the counties with less than 10 licenses like Santa Barbara, Sonoma, Sacramento, and Orange have remained relatively flat over the years. Santa Barbara makes sense for this, with the large farms there, and Sacramento and Orange are next to important large urban areas connected by main highways, so they have a population to produce for. Sonoma is a bit of an outlier. It isn't in the top 10 for cultivation, but seems to maintain a decently stable volatile extraction sector. This is likely due to it's location south of major cultivation counties like Trinity, Humboldt, Mendocino, and Lake. Sonoma sits right between these counties and the Bay, combining cheaper real estate with a decent population of skilled workers and a reasonable delivery distance to Bay retailers.

San Bernardino tops the list of volatile extraction, and at one point was neck and neck with it's neighbor, Riverside. These counties are on the edges of the Los Angeles sprawl, which makes them a decent place to locate a manufacturing facility- close enough to easily deliver to the city, but far enough away to reap real estate and traffic benefits. These neighboring counties diverged heavily in 2023. SB saw a sudden growth spurt, bucking the State trend entirely, while Riverside's downtrend only accelerated. At the beginning of 2026, they are on track to be equal in a year or two.

Some causes for the slightly more stable trend in the volatile sector (ironic...) are the cost, complexity, and specialty of these facilities, as well as their ability to process anything at high volume. Volatile extraction uses large amounts of highly flammable and explosive liquids that need to be stored carefully. A volatile facility needs special containment, backups, fire suppression, and planning permits to build, and as a result are much more expensive. Therefore, these facilities are often only installed by well capitalized operators, who can better afford to keep them open and invest in other opportunities to maintain cash flow in a down market. The other thing that keeps these facilities going is that they can, and will, process damn near any kind of weed- old, dry, boof, etc can be cooked down efficiently with volatiles, allowing these facilities to pull from a wider range of sources to maintain their volume.

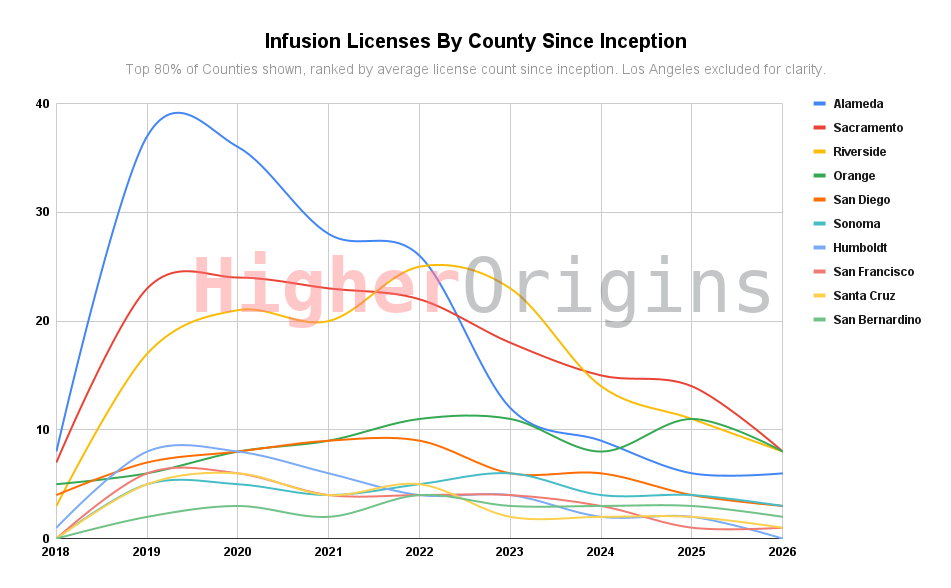

Infusion facilities follow similar trends to volatile extraction, with a few outliers. Here, San Bernardino and Riverside are still showing some weird blips, with Riverside showing serious growth going into 2022, while a few years later San Bernardino saw a more modest bump. The biggest crash by far though has been in Alameda, who has lost around 85% of their licenses. Despite this, Alameda and their sister across the bay in San Francisco are the only counties on an uptrend at the end of the data set, however slight.

Above we discussed the fact that the infusion licenses are being replaced by the non-volatile category who can also do infusion. While that is a trend, another may be the reduction of specialization in edibles. This is mostly anecdotal observation on our part, but edibles have become a lot simpler over the years. Things like cookies, chocolates, and infused treats seem harder and harder to find, while drinks and gummies make up the vast majority of stony snacks. It's a lot easier to produce beverages and gummies at scale than it is to do cookies and brownies. Mixing and pouring gummy goo into molds or liquid drinks into cans is much easier and more repeatable than cookies and brownies. Likewise, for the consumer it could be easier to dose a simple 10mg gummy or a one-can social tonic than a brownie, as we all know from that one time in college. This move towards simpler to manufacture products may have put some more specialty edible kitchens out of business.

Packaging licensing everywhere but LA has crashed hard, with all counties shown having no more than two licenses. Since legalization, Alameda and Riverside lead the category after LA, but these counties were already on a downtrend before the uncertainty of the pandemic, indicating major economic issues for the license type. Packagers can pack products of all kinds, but also many other license types can do their own packaging, so the category faces a lot of competition. With the cost of 3rd party packaging cutting into already thin margins, many operators choose to internalize their packaging if they have the option.

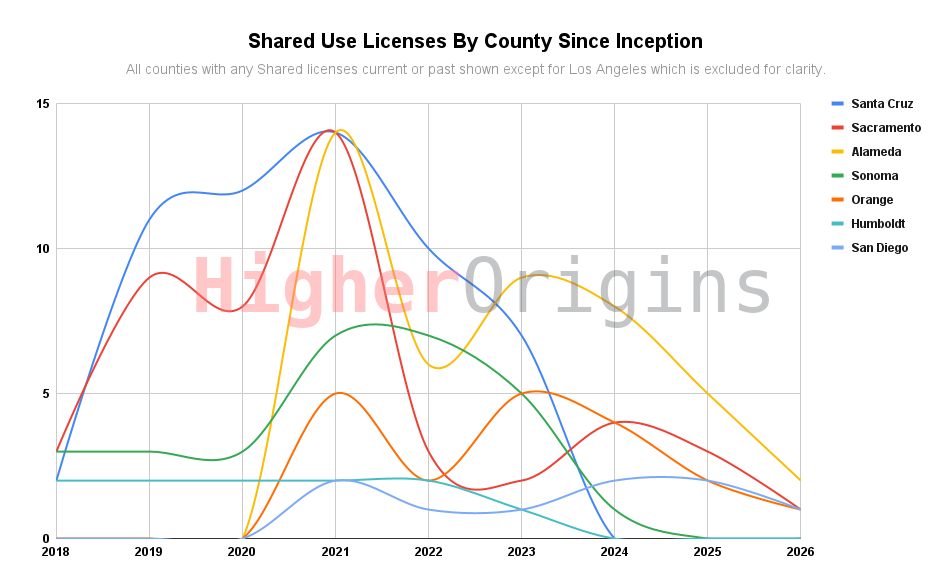

Shared licenses have always been rare, and this chart clearly illustrates it. Shown are all counties that have ever had a Shared manufacturing operation. After a 2021 peak mostly lead by Sacramento, Santa Cruz, and Alameda, the license type has collapsed to only five operations, enough to summarize in a simple list:

Depending on the health of these businesses and how many collaborative-minded brands out there have the capital to combine for a shared space, these may be the last operators of their type in the state.

Who Are The Big Players?

Determining scale of manufacturing is fairly hard to do. There is no scale-based reporting or license sizing to work with here like in cultivation- one manufacturer could make one joint a year or a thousand liters of distillate a month and we'd never know without stalking them. What we can do is look into the manufacturers owned by the biggest operators in the state, as identified in our previous two reports, since they likely have large output.

Heirloom Valley LLC and Ag Roots LLC

These two businesses each make up half of a single Santa Barbara megafarm, making them the largest single farm in the state. Owned by two brothers, likely under the Umbrella of Pro Farms, this operation seems to be entirely cultivation, with zero active manufacturing licenses tied to either brother. They must have a connection to manufacturers in the area or in LA, but we can't be sure which ones.

Another Santa Barbara megafarm, Salisbury Canyon Ranch is owned and operated by LEEF, a business that actually started as a state of the art extraction manufacturer based in our own Willits California. With the massive output of this megafarm, it would not surprise us if their manufacturing license was one of the high-output operations in the state. Due to the logistics of shipping cannabis all the way from Santa Barbara to Mendocino county, it wouldn't surprise us if a significant portion of the weed from Salisbury Canyon is extracted locally or in LA instead.

People's is a truly massive farm in Kings County, dedicated to field grown cannabis, almost all of which is turned into distillate. They operate a volatile extraction license, which they claim is the biggest lab in the state and only uses biomass from their farm. They also operate an infusion license.

This large outdoor farm in Riverside county lacks a lot of public information, and likewise does not seem to be associated with any easily identified manufacturers or even a distribution license. Their product could be manufactured anywhere, and we have no way of determining where.

Healy and Associates LLC and Canyon Produce LLC:

Los Alamos Gardens is a Santa Barbara megafarm operated by QCSC group. These two locations are located nearby each other and operate under the same ownership, so technically together they make up the largest collection of cultivation in the state, although we have no idea how integrated the two megafarms are with each other. This huge conglomerate is associated with three manufacturing licenses:

Since the publishing of our cultivation article, this megafarm has been completely cancelled and seems to have gone under.

GBH, owned by Greenbriar Holdings, is a megafarm in Fresno county. They are associated with one volatile manufacturing license.

This Santa Barbara operation is associated with Central Coast Agriculture, and therefore Raw Garden. They have one packaging license and one volatile license.

Glass House Camarillo Cultivation LLC

This Ventura megafarm complex grows in repurposed vegetable greenhouses. They are associated with a single volatile extraction facility.

Pacific Stone operates this Santa Barbara megafarm, and is not associated with any manufacturing licenses.

Stiiizy/Shryne Group

Stiiizy is a dizzyingly complicated conglomerate of every kind of license, who famously operates with limited public transparency. Due to this, it's not possible to determine what volume their licenses produce. They are associated with the following manufacturers:

This large retail chain has rapidly expanded across the state, lead by their media-savvy owner Elliot Lewis. They are not clearly associated with any manufacturing licenses.

Off the Charts is another large retail conglomerate, who holds one infusion license.

Gold Flora/Stone Blossom Capital LLC

An unstable conglomerate partly owned by a receivership, with three manufacturer licenses:

It's important to note that just because these licenses are owned by big players, doesn't mean that they're actually doing production at the levels they claim. There might be a huge operation somewhere that only has one license, but works with dozens of customers to put out hundreds of products. Manufacturing is by far the least observable aspect of the California industry.

Conclusion

Like all sectors in California's cannabis industry, the manufacturing sector is in the middle of a serious downtrend, with the majority of licenses centralized in Los Angeles county which has a more stable market than the rest of the state. Non-volatile manufacturing is by far the most common type, with volatile extraction a distant second. Infusion is third and falling drastically. Packaging is still going strong in LA but suffering statewide, and shared use licenses are basically extinct. It's difficult to track specifics of manufacturing, since these licenses aren't associated with scale like cultivation, or taxable sales like retail. While large players do own some manufacturing and may claim that they have the largest operations, there's no real way of knowing who the actual biggest manufacturer is within any category. With the downtrends seen in cultivation and commercial markets across the state, there is no clear path to stability for the manufacturing sector, especially for non-vertical smaller operators or licenses that don't already have large reliable clients.

And with that, we've reached the end of our 2025 cannabis insights series! We appreciate your patience with the release schedule of these reports, and would like to thank you for reading. Higher Origins is a cannabis software platform and marketing company based in Mendocino County that specializes in helping get small farms to market. If you are a licensed retailer who is looking to source unique, high quality products and would like to support small farms in these uncertain times, you can sign up for free to order products from a farm. If you are a farm, small or otherwise, who is looking for an easy, clean online system to power your sales, we'd love to work with you and help get your products on shelves!

Thank you so much for reading! If you like what you've seen, check out our YouTube podcast, Instagram, or our LinkedIn for more.

Keep your concentrates clean and your rosin press warm

-The Higher Origins Team

Comments (1)

Great Article!