In our previous article, we took an in-depth look at the California cannabis cultivation sector, from the start of legalization to the beginning of 2026. While extremely interesting, cultivation is only the first step in the process: cannabis has to be tested, transported, distributed, and sold, all of which falls under the commercial category of California’s State licensing program. In this installment of this three-part series of analytics reports, we will deep dive into this commercial sector and bring you up to date on how it has evolved since legalization.

The dataset used in these analytics reports comes directly from the California DCC’s Cannabis Unified License Search. This is all publicly available information, we’ve just taken it and made it more user friendly. If you would like to browse the data, we recommend our License Search, which offers a more searchable and user-friendly alternative to the State’s search. You can also use our new “Summarize” button on any search to access a variety of graphics and data visualizations.

A note on some of these charts: for clarity, we've included only the top 80% of counties in most charts, for clarity. California has 58 counties, and including them all would make the charts too packed to read easily. Please consult the subtitle of the charts to see what was omitted.

Now, on to the report!

Overall Commercial Licensing

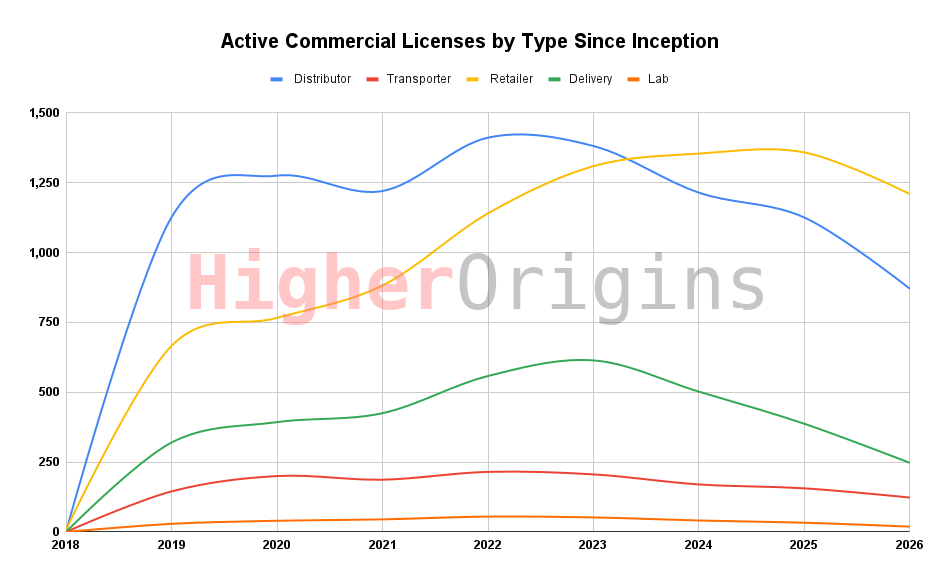

Commercial licensing opened up with the rest of California’s cannabis licensing in 2018. Immediately, tons of people rushed to get distribution licenses, some for personal use of their own business, but many for the opportunity to be able to secure an early market advantage. The distribution license essentially functions as a State-mandated middleman. Cannabis must be legally transferred to a distributor from a farm before it can be moved to retail. On paper, these licenses were meant to be a mechanism for easier regulation and logistics, but in reality they can be operated purely for arbitration- buying low, selling high, gatekeeping the market, and in the worst cases, taking in cannabis from farms and never paying them back. Regardless of their intentions, distribution was the strongest growth category at the beginning of the legal market in California.

As time went on, the distribution market got rocky. Some early opportunists failed, while others got bought out in the inevitable wave of market consolidation. Many cultivators who had gotten a distro license just to manage their own product went out of business. Issues with non-payment began to plague the industry, and haven’t really gone away. Retailers would refuse to pay distros, and distros would refuse to pay farmers. The reputational backlash of all this revenue theft drove some particularly exploitative distros out of business. Still others disappeared suddenly after buying up a lot of inventory, much of which ended up unaccounted for. These disappearing distros are known throughout the industry as “burner distros”- licenses which exist solely to launder products in or out of the industry for illicit profit. License loss has affected even the biggest players in the distro space. Dominant brands like HERBL have flamed out spectacularly, leaving the market contagion of millions of dollars of unpaid revenue in their wake.

In 2023, distro licensing fell below retail as the most popular commercial license in the state. Big players like Nabis started to consolidate the market, while more unstable distros and those associated with failing smaller cultivation operations went under. Currently, distribution is on a solid downtrend with the rest of the industry. Over time, we expect that distros will become a much smaller and more consolidated sector, just like in other industries where a small group of broker/warehousing/logistics businesses service many more retail locations.

Naturally, all these distros need to be able to sell their weed to someone, so retail licenses were the second most popular license for people to get when the market opened up. Since California’s cannabis rules are subject to additional regional/county/municipal rules, many areas have significant cost, red tape, and taxation associated with opening a new dispensary. Depending on the area, a licensee could easily be looking at hundreds of thousands of dollars in added costs on top of the building, lease, and State fees, not to mention extended timelines due to application backlogs or obstructionist local bureaucrats. Some jurisdictions prohibit cannabis sales altogether.

Another reason why retail was slower to grow was that nobody really knew what the market was going to look like, so for the first year or two everything was really speculative. You can see this trend play out over time in the chart- those with the cash and risk tolerance jumped in early, opening around 750 dispensaries right off the bat. After that, as more cautious investors entered the market, the number of retailers crept up more gradually.

Despite heavy local taxes and red tape, retail kept growing all the way until last year, when the downward pressure on the rest of the industry, likely coupled with inflation, started to catch up. With several large brands entering receivership and the illicit market still providing the majority of the weed in the state to increasingly cash strapped consumers, retail is feeling the pressure as well. Big players have consolidated control, especially in larger urban areas, and their similar inventories of predictable big brand commodity products have started to standardize the weed buying experience for the average legal consumer.

Delivery licenses (or “Retail-Non Storefront” licenses as the State calls them), pretty closely matched the trend of retail, just at a much smaller proportion. Delivery faces even more local regulation, and comes with the increased overhead and liability of managing last mile logistics. In 2023 some big names in delivery failed spectacularly, which, combined with the slimming margins as prices dropped and inflation rose, sent delivery into a downtrend which has held steady ever since.

Transportation licenses were never very sexy, only existing as a logistical option to move weed around. After a modest peak in 2022, these practical licenses have dropped proportionally alongside everything else.

Testing labs have always been a very small commercial category, since one lab can serve many clients and they are expensive to set up, requiring specialized equipment and qualified laboratory staff. Labs have always been under fire for suspected fraud schemes like “lab shopping”, where labs will allegedly artificially inflate the THC% results of a sample in exchange for an illegal fee, which increases the sales value of the product. Likewise, scandals around improper handling and reporting of contaminated samples have also damaged the lab sectors reputation. In recent years, the State has passed further regulations on labs, which has likely contributed to the declining number of licenses since the peak in 2022.

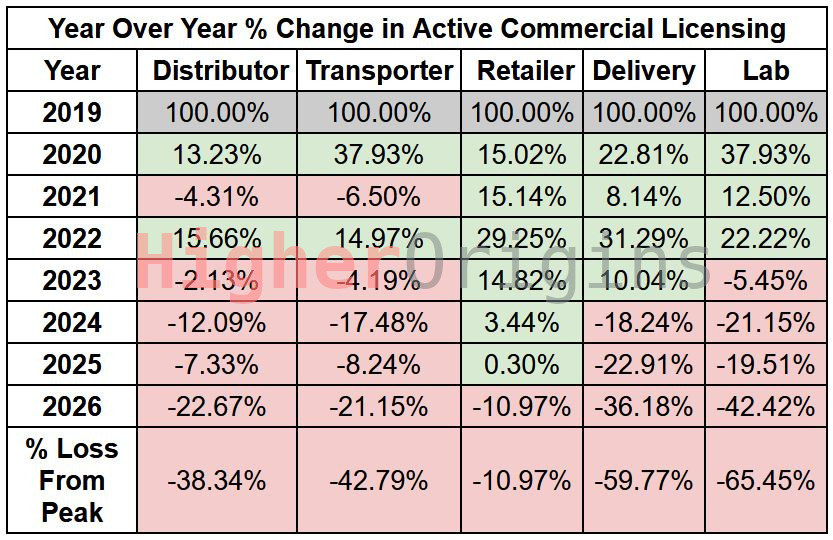

This table shows the percentage changes year over year in the different categories of commercial licenses. Labs and delivery have seen the largest proportion of losses from their peak.

Retail Licensing

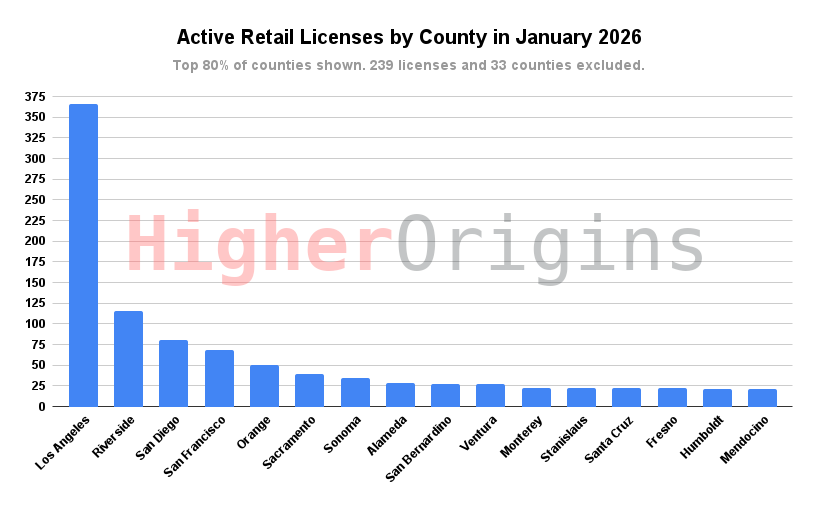

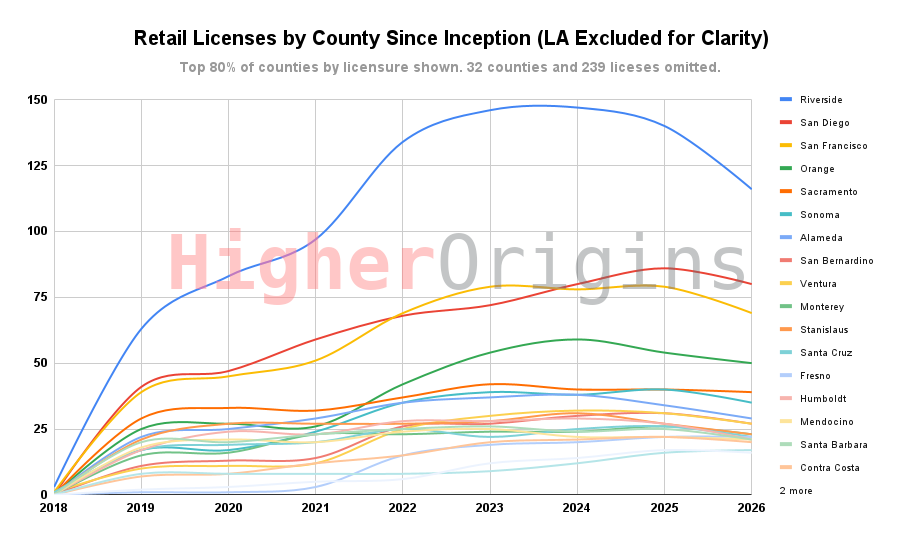

Diving into retail, we immediately encounter the massive whale that is LA, a common theme you will see throughout this report. The megacity holds the most licenses of any county by far, three to four times that of what its distant competitors Riverside and San Diego have actively licensed. While LA County has approximately 25% of the total California population, it has 30% of the state’s active retail locations. LA has more retail than the next 5 counties combined. After LA, only Riverside has more than 100 retailers. For obvious reasons, retail scales proportionately to population.

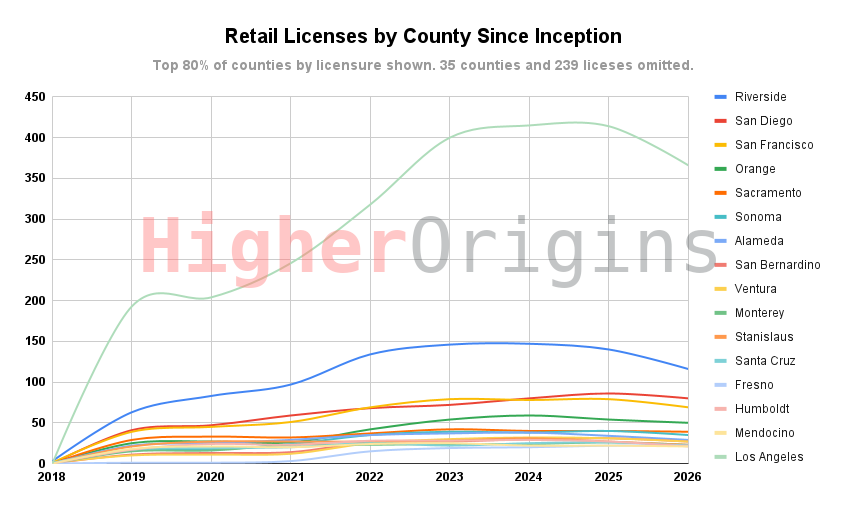

As usual, LA dominates the market trends over time for retail. After an initial boom, the market there corrected in 2019-20 but soon stabilized, leveling off around 2023-24 and finally beginning to shrink last year. LA is so dominant that it makes this chart a bit hard to read if you’re interested in other counties. Let’s fix that.

With LA excluded, the chart opens up a bit to more easily see trends across the rest of the market. Riverside grew rapidly early and then slowed in 2021 before entering a nice parabolic trend that peaked in 2023. If this trend holds strong, Riverside will lose at least a third of its retail locations from market peak. While San Diego and San Francisco were similar going into 2020, they have flip flopped back and forth ever since. At the start of this year, we see San Francisco falling behind, although both are on a similar downtrend. Orange county seems to have peaked in 2024, and has likewise entered into a slow downtrend. The rest of the counties seem to have peaked around 2023-24 and are now level or trending downward, clustering around 20-30 licenses each.

Distribution Licensing

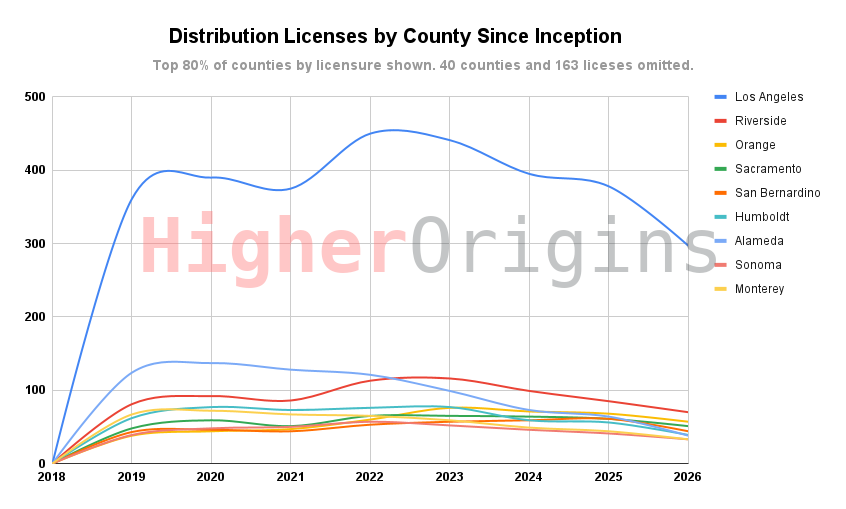

Los Angeles is just as dominant in the distribution sector as they are with retail. All those stores need someone to bring them products from the farms throughout the state, so this makes sense. Riverside, San Bernardino, and Orange counties surround LA, and their large distribution populations round out the regional cannabis logistics. Likewise, Sacramento and Alameda have large populations and grow large amounts of indoor cannabis, so distros make sense in those areas to keep the transfers moving. Humboldt’s remote location with the second largest cultivation canopy in the state likewise justifies a large amount of distros, since all that Emerald Triangle weed needs to get packed and organized for export. One county that surprisingly isn’t in the top 80% is Santa Barbara. It seems that the county with the most cultivation defaults to running most of its logistics through LA where most of their customers and manufacturing is located. Also notably absent is Tulare, home to Nabis’ gigantic distribution facility, likely the largest in the state. It seems that Vince and Jun picked Tulare for its central location rather than any existing large distribution industry.

The dip in licensing in LA that started after the initial post-legalization growth lasted a year longer for distribution than it did for retail. In general, distribution peaked earlier and began to trend downwards earlier than retail. This makes sense, as the distro sector has been plagued with many failures, and over time more established and efficient companies have consolidated their control, putting shakier competitors out of business. Likewise, there is just a lot less weed to distribute, since cultivation is down over 50% from its peak in some categories.

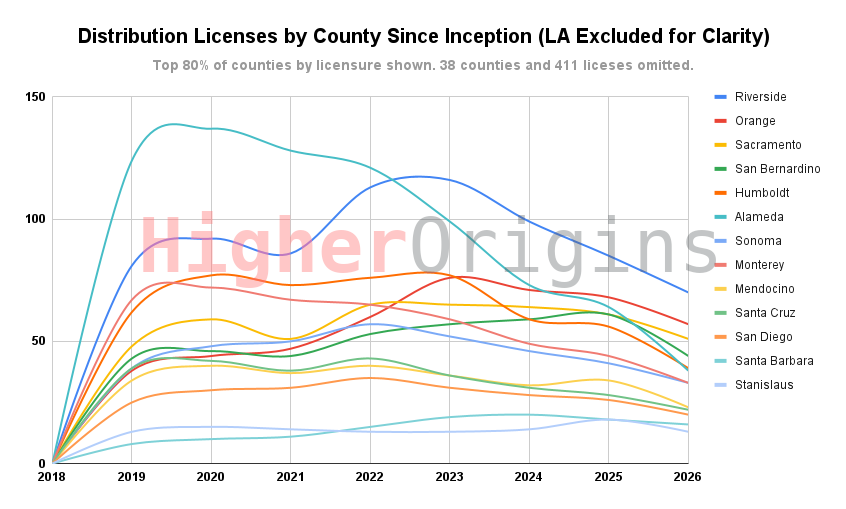

Removing LA from the chart gives us a clearer picture of the smaller counties distribution markets. Every single county is on a downtrend, with Alameda falling off the hardest, losing just over two thirds of its licenses. Riverside had a nice pump in 2022-23, but has been steadily declining ever since. If trends continue, soon no county other than LA will have more than 50 distributors. With LA removed, Santa Barbara is now visible, and is one of the most stable counties, which makes sense considering it has the largest crop in the state. The sheer mass of megafarm product it grows and exports can easily keep a handful of distros open. The third largest cultivation county, Lake, fails to make the top 80% even with LA excluded, indicating that there is a mismatch there between local logistics and production.

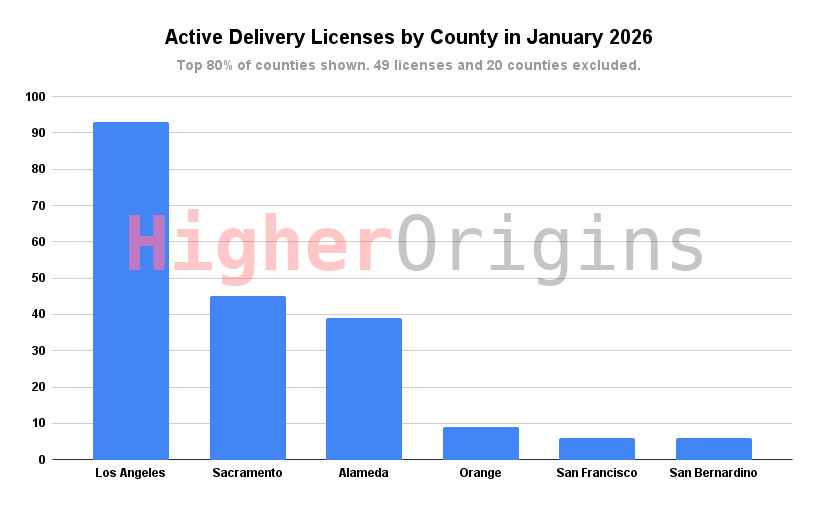

Delivery Licensing

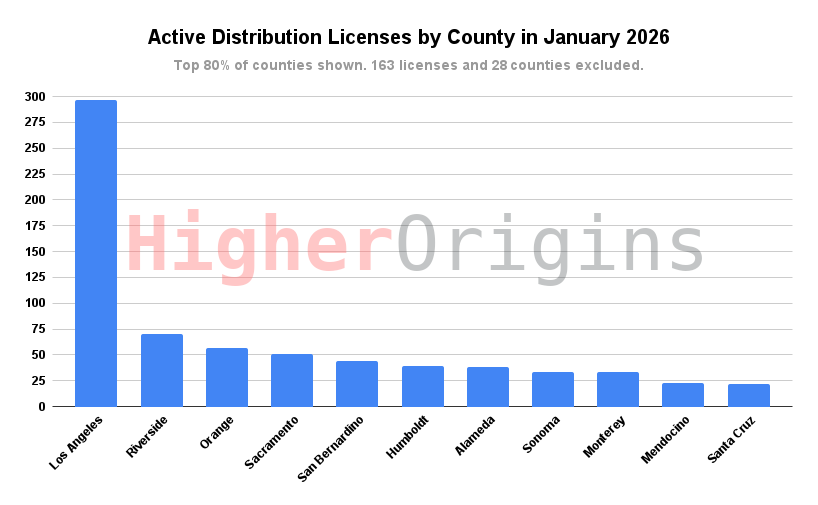

LA leads the pack again in the delivery category, but it’s much closer this time. Sacramento comes in second with just less than half of what LA offers, a massive proportional shift considering the roughly 1.5/10 population difference between the counties. Alameda covers the East Bay with just under 40 services who will deliver weed. The OC, SF, and San Bernardino fill out the top 80%. As expected, delivery is dominated by urban areas with the road network, population density, and capital to enable services to squeeze out a margin in California cannabis’ most ravaged sector.

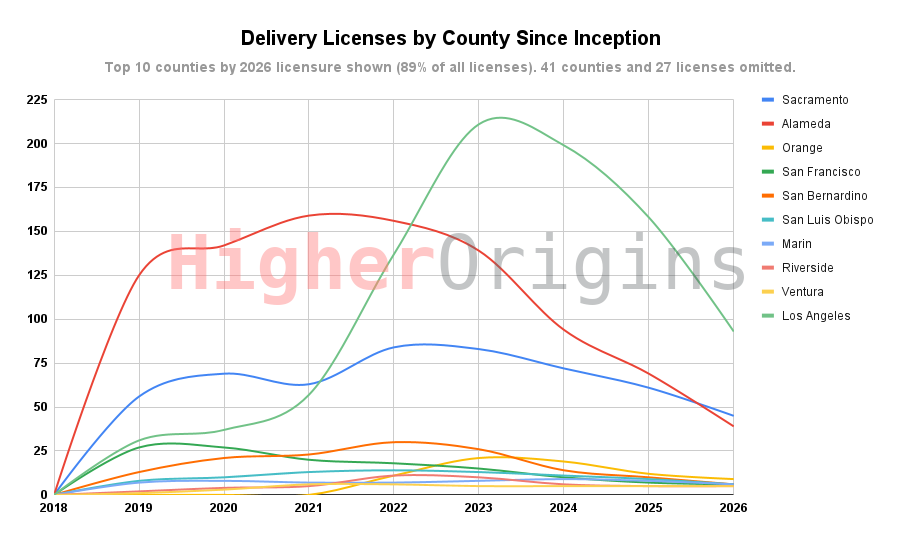

The delivery market statewide is rapidly plunging to a flatline. The top three urban areas that serve as epicenters for delivery companies are falling sharply- in LA, the boom and bust cycle looks like it will be complete by the end of 2026 or sometime in early 2027. Every other county outside the top 3 has settled in with 10 or less delivery services. These failures are likely due to the massive overhead costs of running a delivery service, coupled with competition from brick and mortar retail, the more successful illicit market, and cash strapped customer’s unwillingness to pay extra to have their weed delivered.

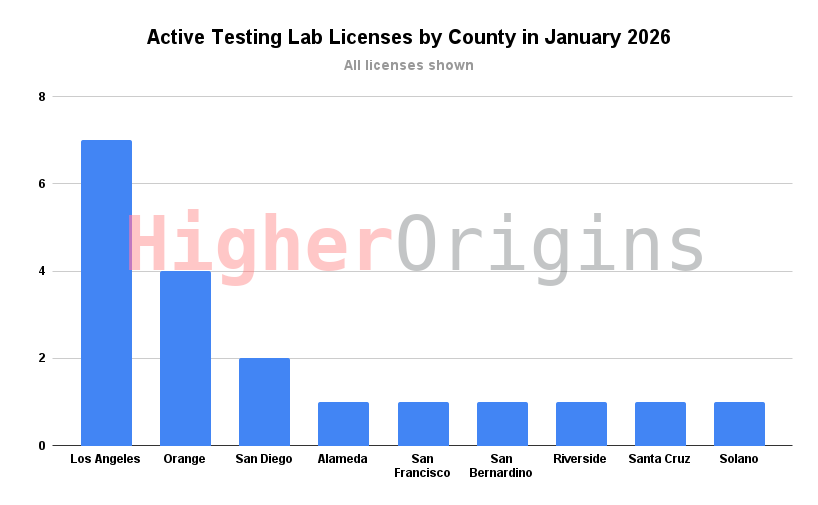

Testing Laboratory Licenses

Labs are a small but important category. Every single cannabis product on California shelves must be tested, which requires special equipment and technically skilled lab staff. Naturally, these labs cluster in urban areas and near centers of distribution.

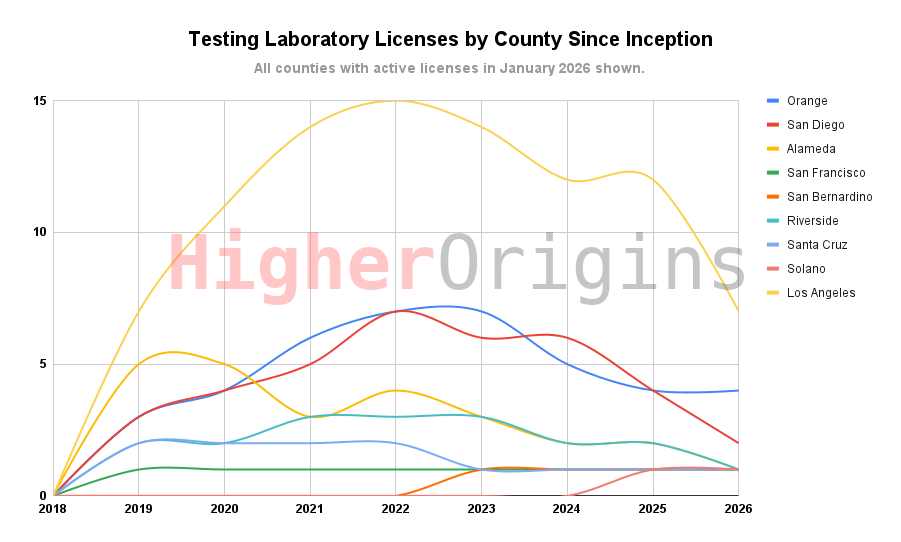

The laboratory sector is small, but still has volatility. Alameda and San Diego particularly have had some ups and downs over the years. In 2024, new rules on testing were passed, which increased the barrier to entry for labs and made many fail. This started a statewide downtrend that has only really stabilized in Orange County.

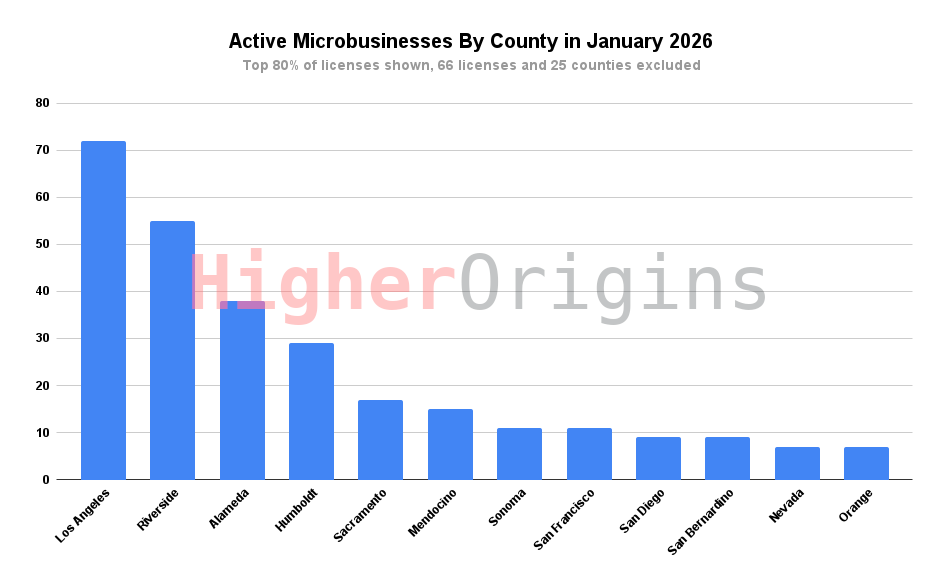

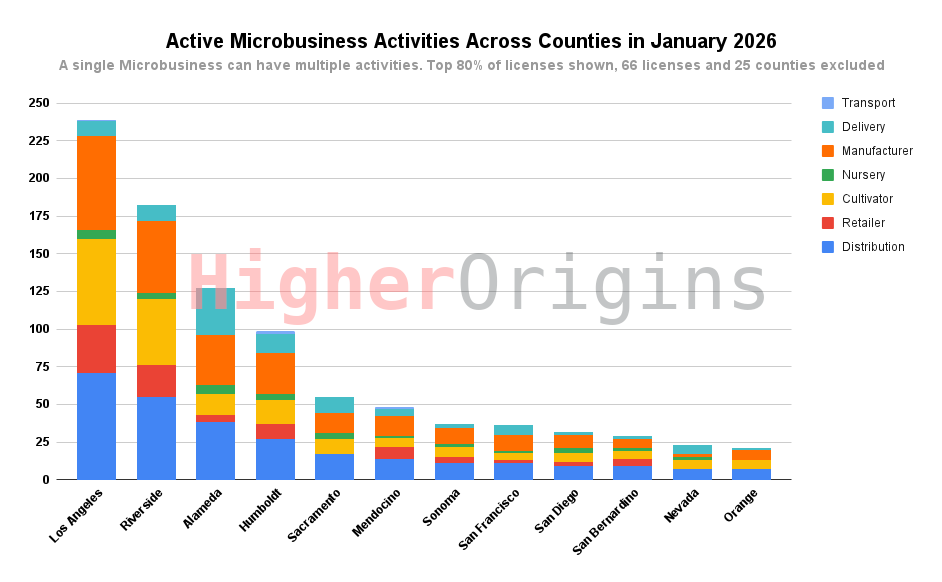

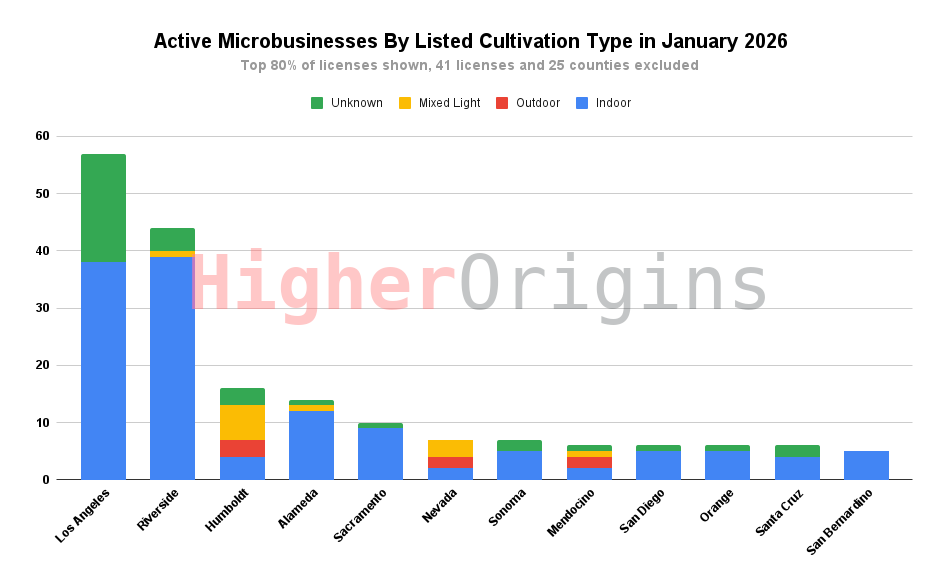

Microbusiness Licensing

Microbusinesses are a strange category. These licenses act like legal Swiss Army Knives, allowing a licensee to do a little bit of everything. As such, they usually get less attention because it is hard to observe exactly what category they actually fit into. In the past year, the State has gotten better at reporting microbusiness activity, so we can finally start to explore what these licenses are up to.

Since space is at a premium in cities and most cultivation there is indoor, it makes sense that microbusinesses would be a popular solution in urban areas. The more you can vertically structure your business to have more steps under one roof, the less expensive city real estate you need to rent. Likewise, if you live in a cultivation focused rural area like Humboldt or Mendocino, a microbusiness can allow you to do more of your manufacturing in house, rather than rely on expensive, far away third parties to get your market retail ready.

Each microbusiness license can be associated with multiple activities. Regionally, the breakdown of activities seems fairly proportional, with a few small exceptions. Alameda micros are more likely to run a delivery service, but less likely to operate dispensaries. This trend continues East along the Capitol Corridor to Sacramento, where there are no microbusiness brick and mortar retailers.

The microbusiness cultivation crop is dominated by indoor, except in more rural areas like Humboldt, Mendocino, and Nevada counties. We’re not sure why some micros have no cultivation type indicated on their licenses- likely this is due to gaps in DCC record keeping.

Big Businesses

Who are the biggest commercial brands in California? This is a complicated question. Unlike cultivation where one business name is associated with many licenses, retail and distro operations are all recorded under different business names, so it’s harder to total up a retail brand’s total number of stores. In some cases, they all have the same name, in others they have different names but all source the same product, and others still all seem to be completely unrelated at first glance. Likewise, large distros might have only a few licenses but those might be huge warehouses or factories. The most reliable connection between different businesses is their ownership. By adding up the number of active licenses owned by each of the top 5 retail owners in the state, and associating their brands together as best we can, here’s what we’ve learned.

Stiiizy/Shryne Group

Vivian Khong, James Kim, Isaac Kim, Tak Sato, Chaudry Ali

Split between 5 major license owners, we have the mega conglomerate that is Shryne Group, AKA Stiiizy. This multi state operator is the largest weed brand in the world, and, according to Forbes, 1 in 8 legal weed products sold nationwide have their label. In California, at least 58 active licenses are listed under the ownership of their partners. Stores like Shryne, SGI, Authentic, Ironworks, and others are under their ownership. Exactly how Stiiizy operates has always been a little unclear as they rarely talk about their operations and seem to favor anonymity. For a brand well on its way to hitting billion dollars in annual sales, it’s shocking that Shryne Group’s website is dead. What is clear is that they have been often accused of bending or breaking the rules in multiple states, although no existentially threatening charges have stuck and their brand continues to grow rapidly nationwide with massive success. Since Stiiizy has been around since the very beginning of California’s legalization its owners, and its associated licenses of all types, are basically a load bearing part of the state market. It’s hard to do any brand or license research in California and NOT have them come up in the search results.

Elliot Lewis, Damian Martin

While Stiiizy doesn’t like to put themselves out there, the owner of Catalyst is the polar opposite- Elliot Lewis, known for his passionate videos where he aggressively calls out alleged bad actors with high profile lawsuits. Lewis has been rapidly expanding his company throughout the state under the slogan of “Weed For The People”. Catalyst started in Long Beach, and now holds at least 33 active commercial licenses statewide. While Lewis acts as a vocal frontman and is always trying new ways to set an example and call out problems he sees in the industry, like all big cannabis brands, there’s limited transparency of how the company operates under the hood, as we found a while ago when we tried to track down the source of one of their products.

With 33 active licenses statewide to his name, Norman Yousif, owner of the Off The Charts chain of dispensaries, seems to be in close competition with Catalyst. Their site claims that they are a family business, and they have even opened a noteworthy lounge in LA. Beyond that, there’s not much information on Off The Charts, or OTC as they often refer to themselves as. Norman doesn’t seem to seek the spotlight, but a leaked video in 2024 gave him some significant bad press when he was caught on camera bragging about not paying small operators.

Kevin Singer

This one is a little different. While all the other top owners actually started out trying to run cannabis businesses, Mr Singer is the one who steps in when they fail. Singer is a court-appointed Receiver, meaning that when a cannabis company goes under, he is given control of the companies assets and licenses in order to stabilize and sell them to the highest bidder to pay off the companies debts. Due to the frequent failure of cannabis businesses in CA and the large debts involved, Singer has been quite busy. Currently he is named as the owner of 33 commercial licenses statewide. As of the beginning of 2026, he holds licenses from Element 7, Harborside, Urbn Leaf, Loudpack, and others.

Gold Flora/Stone Blossom Capital LLC

Richard Ormond, Greg Gamet

Gold Flora is a large house of brands company that controls a variety of retail locations around the state, including Coastal, Calma, and Deli by Caliva. This company is a conglomerate, Frankensteined together by Stately using parts of The Parent Company, Caliva, Airfield (which is now associated with Stiiizy), and others. Currently, Gold Flora is in receivership, under Richard Ormond of Stone Blossom Capital. You can listen to Richard talk about his role here. At the moment, 16-20 licenses seem to be part of the brand. We encountered a Gold Flora product from the Gramlin product line last year in this article.

And with that, we reach the second of our three reports on the California cannabis industry. In this installment, we’ve taken a look at the state of commercial licensing across the state, from the start of licensing in 2018 to the current landscape in early 2026. The downtrend across the industry that has been going strong for the past few years has hit the commercial sector just as hard- from plummeting delivery licenses, to consolidating distribution, to a more recent drop in retail, the market across the board is shrinking dramatically. We expect this trend to be just as visible in our next installment on manufacturing.

Despite these losses, large players have continued to carve out their corners of the market and consolidate their competition. We’ll be deep diving these big players even more in another upcoming article. Stay tuned for that as well!

These articles serve to keep everyone involved in California cannabis informed. In an industry plagued by bad information and short term decision making, we feel that publishing even these limited insights is worthwhile to keep everyone up to date. Thank you for reading!

Higher Origins mission is to get as many small farms to market through financially sustainable supply chains as possible. Our marketplace, menus, marketing, brand, and platform tools serve to connect buyers with small farm sellers and promote sustainable business practices. Interested? If you hold an active CA cannabis license, you can sign up today to shop or promote your product for free. You can keep up with us elsewhere as well, via our YouTube podcast, Instagram, or on LinkedIn. Questions? Hit us up anytime at [email protected]

Thanks for reading and keep growing!

-The Higher Origins Team

Comments (0)

No comments yet. Be the first to join the conversation!